The 62-Year Scorecard

There comes a season of life when the questions change.

Somewhere around age 62 — about the time many people begin thinking seriously about retirement — the focus shifts. The conversation moves from accumulation to preservation, from maximizing growth to ensuring durability. The question is no longer, “How much can I build?” but rather, “Will this last?”

This is a natural shift, but it also represents a moment when investors are vulnerable to forgetting the most important evidence available to them: their own lived experience.

This led me to create a tool to help clients recognize the value of those experiences; I call it the 62-Year Scorecard. It asks a straightforward, honest question: What has actually happened over the course of your lifetime? The intent is to put all the events of an investor’s lifetime into perspective. Often, the answers are surprisingly comforting.

Imagine you were born in 1963. To celebrate your arrival, your parents did two simple things. First, they purchased one share of the S&P 500 for roughly $65 and tucked it away (those didn’t exist yet, so this is just an example.) Second, they invited all their friends and family over to celebrate your homecoming from the hospital. In preparation for the party, they stocked the kitchen with milk, bread, meat, cereal, produce and other ordinary groceries totaling about $30.

Now, fast forward 62 years.

That single “share” of the index is worth just under $7,000, roughly a hundredfold increase in value. The dividends paid by that same share have grown from about $2 per year to nearly $80 per year, almost 40 times higher. Meanwhile, recreating that $30 grocery basket would now set you back over $300.

In one lifetime, three forces quietly did their work: Productive businesses grew substantially in value, the cash those businesses paid their owners rose meaningfully over time, and inflation steadily increased the cost of living.

Everything else — the headlines, the elections, the crises, the recessions — was noise.

And those 62 years had an awful lot of noise. Six decades revealed oil shocks, double-digit inflation, the crash of 1987, the dot-com collapse, the financial crisis of 2008, a global pandemic and repeated warnings that markets were headed for permanent decline. Prices were cut in half more than once. At various points, the outlook seemed bleak.

Yet the scorecard continued to advance. It wasn’t smooth or predictable, but it was persistent.

This matters because retirement planning is not about any single year. It is about decades.

As investors approach retirement, the questions that truly matter become surprisingly straightforward: Have I accumulated enough to live independently and with dignity? Will my income keep pace with the rising cost of living? For many families, there is a third, quieter question as well: Will there be something left to help my children or grandchildren when they need it most?

The 62-Year Scorecard does not guarantee outcomes, but it provides context — and context is often what tempers fear.

Over an entire lifetime (the past 62 years, for example), ownership of productive businesses accomplished three critical objectives:

- It built real wealth after accounting for inflation.

- It generated rising income.

- And it adapted to higher living costs.

That second point deserves emphasis. Retirees do not spend portfolio balances; they spend income. Over the past six decades, dividends did not sit idly; they grew, often at a pace that exceeded inflation. For retirements that are now stretching to 20, 25, or even 30 years, that growth is essential.

And yet, ironically, the closer people move toward retirement, the more tempted they become to abandon the discipline that carried them there. Short-term market volatility begins to feel more dangerous than long-term inflation. Temporary declines are mistaken for permanent loss. The familiar phrase “this time is different” begins to sound persuasive.

The scorecard reminds investors of a counterpoint: You have already lived through the difficult periods, and the strategy endured. Time rewarded patience.

Markets will fluctuate, inflation will persist, and uncertainty will remain part of the landscape. But when viewed across an entire lifetime instead of a news cycle, the evidence becomes clearer: Ownership of productive businesses, given sufficient time, has historically created wealth, generated growing income and defended purchasing power.

The 62-Year Scorecard is not about nostalgia, but perspective. That perspective, grounded in your own lifetime, may be among the most valuable assets you carry into retirement.

About the author

Steve Booren is the Owner and Founder of Prosperion Financial Advisors, located in Greenwood Village, Colo. He is the author of “Blind Spots: The Mental Mistakes Investors Make” and “Intelligent Investing: Your Guide to a Growing Retirement Income” and a regular media columnist. He was recently named a Barron’s Top Financial Advisor and recognized as a Forbes Top Wealth Advisor in Colorado.

To schedule a conversation with Steve, visit https://prosperion.us/contact/

Securities and advisory services offered through LPL Financial, a Registered Investment Advisor, Member FINRA/SIPC

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual.

The Last Kind Words

Sponsored Feature

sponsored-feature@denvergazette.com

Updated 4 weeks ago

A saloon, a novel, and the legacy of the American West Filled with curios of a day gone by, The Last Kind Words Saloon is a window to the legendary Wild West. It’s hard to imagine the travails of pioneer...

Sponsored Feature

Reporter

Your Plan (and Behavior) Matter More Than the Headlines

Steve Booren

steve-booren@denvergazette.com

Updated 1 month ago

Early in each year, I like to refocus on what actually drives long-term investment success. The highest returns aren’t from correctly guessing what the market will do, and they certainly don’t come to investors who react to the day’s loudest...

Steve Booren

Reporter

Where the Wind Takes You: Inside the Allure of Windstar’s Small-Ship World

Sponsored Feature

sponsored-feature@denvergazette.com

Updated 2 months ago

The first hint that you’re not on a typical cruise comes long before the ship sails away from the pier. It happens the moment you step aboard — no jostling crowds, no echoing announcements, no endless hallways vanishing into anonymity. Instead, you’re greeted by name, handed a cappuccino...

Sponsored Feature

Reporter

Anchoring: The Mindset Mistake That Quietly Steers Investors Off Course

Steve Booren

steve-booren@denvergazette.com

Updated 2 months ago

I meet monthly with thoughtful, experienced investors who genuinely seek the best decisions. Despite any savviness, however, they often fall prey to a similar mental trap: anchoring. It’s not one of ignorance but of human nature. Anchoring is the tendency...

Steve Booren

Reporter

A Desert Icon Blooms

Sponsored Feature

sponsored-feature@denvergazette.com

Updated 2 months ago

A $200 million transformation elevates The Oasis at Death Valley into an extraordinary retreat. Just beyond the Nevada-California border at Death Valley Junction, Highway 190 stretches west in a nearly straight line. Flanked by rocky slopes and desert scrub, the...

Sponsored Feature

Reporter

‘Tis the season for sustainability

Sponsored Feature

sponsored-feature@denvergazette.com

Updated 2 months ago

Your holiday style should deck the halls, not the landfills! Our Colorado winter wonderland is dotted with twinkling lights, holiday decor, and table settings. People are meeting, greeting, and shopping for presents to give friends and family in celebration of...

Sponsored Feature

Reporter

Decorating Your Home for a Winter Wonderland

Sponsored Feature

sponsored-feature@denvergazette.com

Updated 3 months ago

Winter decorating isn’t just about the holidays—it’s about capturing the beauty and tranquility of the season, too. With the right colors, textures, and accents, you can create a cozy retreat that feels fresh and inviting without any jingle bells. Think...

Sponsored Feature

Reporter

Current Events Only Raise Uncertainty

Steve Booren

steve-booren@denvergazette.com

Updated 3 months ago

Every investor I’ve met has, at some point, asked a version of this question: “Given what’s going on right now, what should I do?” As a financial advisor, I always consider this a reasonable thought. The world is unpredictable:...

Steve Booren

Reporter

Sailing with the Stars

Stacey Maclachlan

Stacey-Maclachlan@gazette.com

Updated 3 months ago

Windstar Cruises’ Star Seeker and Star Explorer Open New Horizons Imagine waking up to a new horizon every day. Sipping coffee on a private veranda as a sleepy coastline greets the sunrise — whether it’s whales breaking the surface in...

Stacey Maclachlan

Reporter

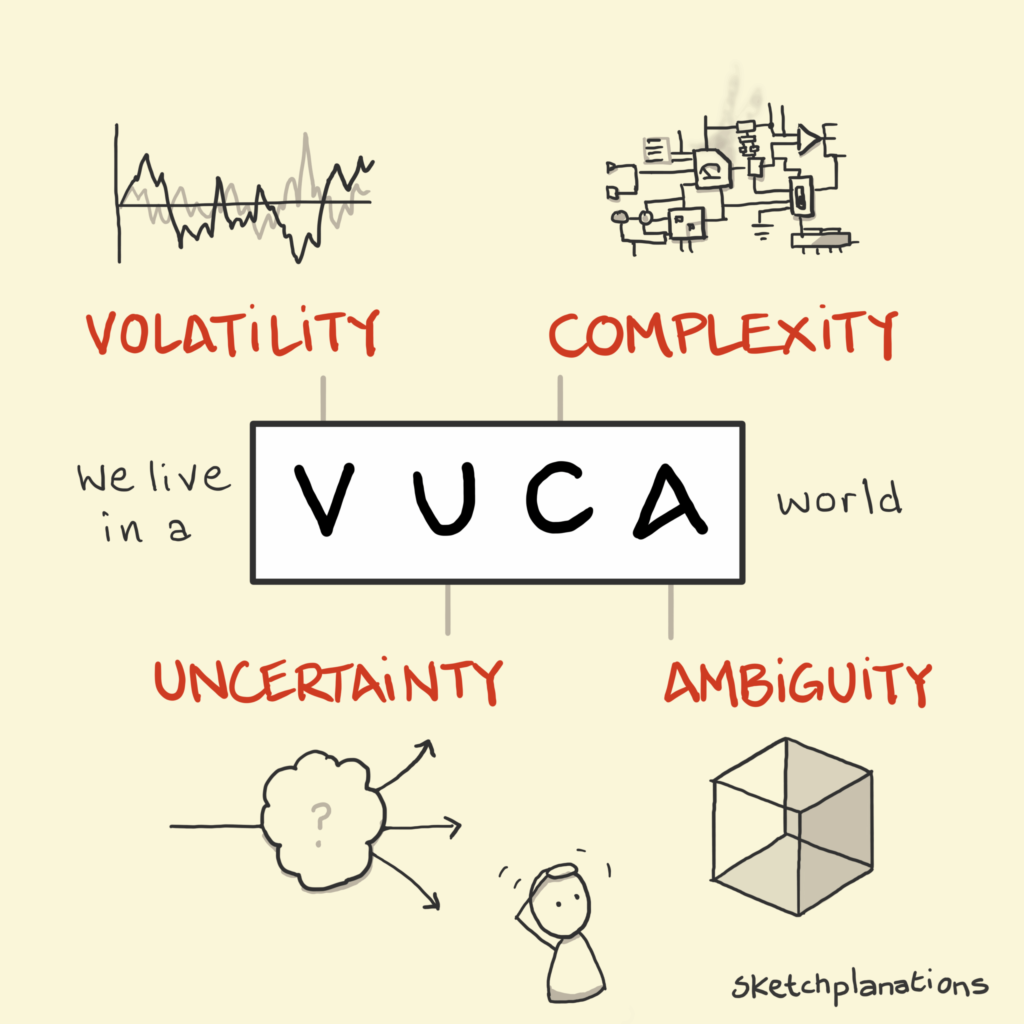

The Antidote to Ambiguity

Steve Booren

steve-booren@denvergazette.com

Updated 4 months ago

Toward the end of the Cold War, a new kind of landscape emerged — defined by turbulence, ambiguity and interconnection. In that moment, folks at the U.S. Army War College coined the term VUCA, an acronym for Volatility, Uncertainty, Complexity and Ambiguity. It...

Steve Booren

Reporter